Dealer Reinsurance and Profit Sharing Programs: A Comprehensive Guide to Wealth-Building for Auto Dealers

- Michael Dean Aufmuth

- Aug 18, 2025

- 5 min read

Updated: Aug 22, 2025

Dealer reinsurance and profit-sharing programs have become essential tools for modern auto dealerships aiming to boost F&I profitability and build long-term wealth. By participating in automotive reinsurance – essentially owning or co-owning the underwriting of F&I products – dealers can recapture profits that would otherwise go to third-party insurers. These profit-sharing programs not only increase a dealer’s bottom line but also offer significant tax advantages, compliance benefits, and opportunities for scalable wealth creation.

In this comprehensive guide, we explain what dealer reinsurance is, why profit sharing matters for dealerships, and how various reinsurance structures (CFC, Super CFC, NCFC, DOWC, etc.) work. We’ll also address common dealer pain points (like compliance and administrative burden) and highlight the real benefits in terms of tax efficiency, customer satisfaction, and wealth-building (see our Dealer Wealth Programs for more on dealer wealth creation).

What is Automotive Reinsurance?

Automotive reinsurance refers to a dealership’s participation in the insurance risk and profits of the F&I products it sells. In a traditional setup, when a dealer sells a vehicle service contract or GAP insurance, a third-party insurance company takes on the risk and pockets any underwriting profit. Reinsurance flips the script: the dealer sets up or partners in a reinsurance company that assumes the risk for those products, allowing the dealer to share in the underwriting profits and investment income from the premiums.

By embracing reinsurance, a dealership gains greater control over its F&I products and how claims are handled. Instead of sending all premium to an outside carrier, the dealer’s reinsurance entity retains the premium reserves in an account the dealer owns. Over time, if claims are lower than expected, the dealer’s reinsurance company keeps the surplus as profit.

Why Profit Sharing Programs Matter for Dealerships

Profit sharing programs unlock an additional profit center for dealerships – one that can be as critical as vehicle sales or service revenue. Here’s why they matter:

Capturing Underwriting Profit: Profit sharing allows the dealer to participate in underwriting profit, turning F&I products into a significant ongoing revenue stream.

Long-Term Wealth and Stability: These programs build wealth over time, creating reserves that can stabilize operations during downturns and fund growth opportunities.

Tax Advantages: Depending on structure, profits can be deferred, taxed at lower rates, or even grow tax-free for years before distribution.

Customer Satisfaction & Control: Dealers with reinsurance have a say in claims handling, ensuring quicker payouts and better customer experiences.

Compliance and Risk Management: Properly structured programs are compliant and secure, helping dealers enhance profits without regulatory headaches.

In short, profit-sharing and reinsurance programs allow dealers to stop leaving money on the table and turn F&I into a long-term wealth-building strategy.

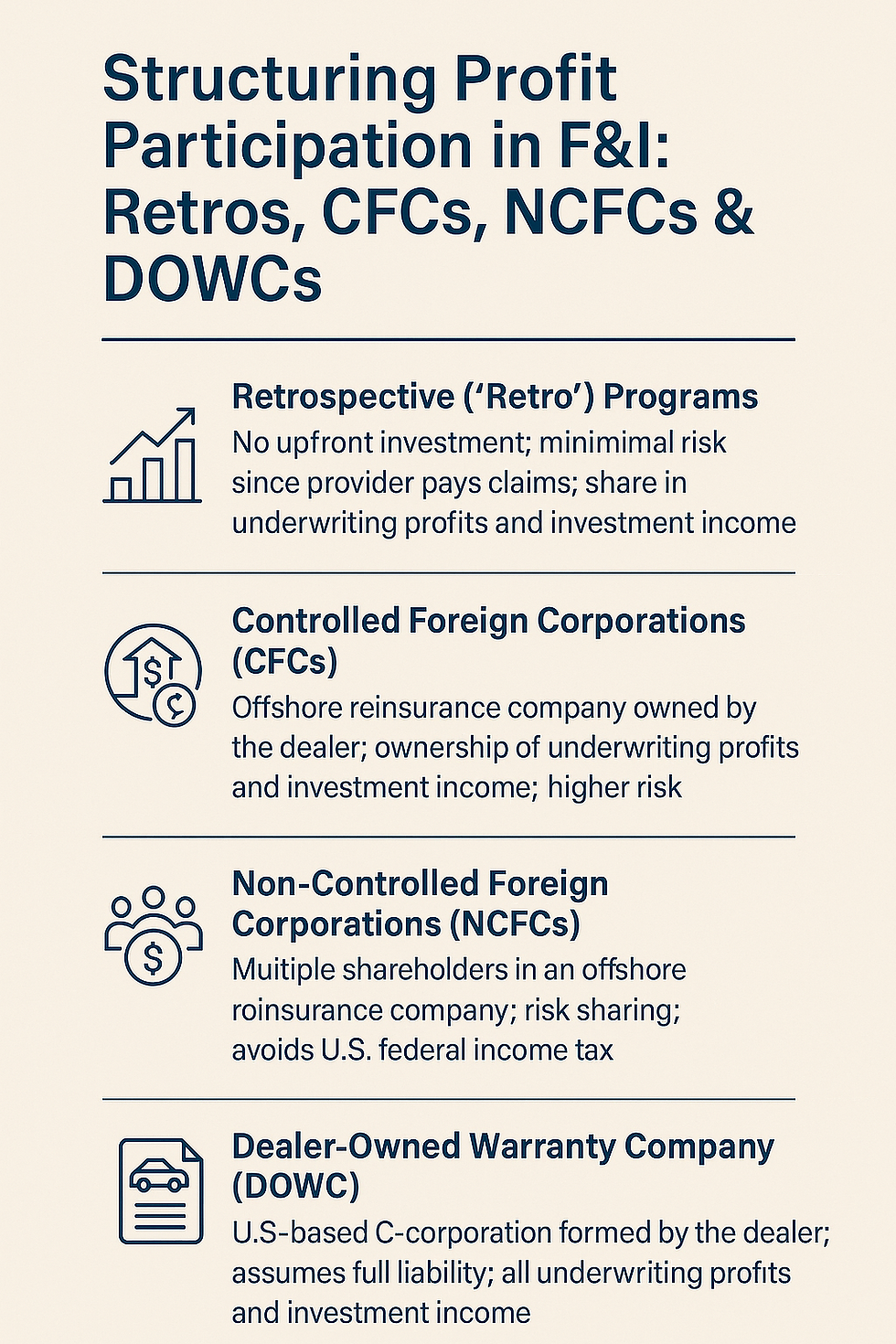

Comparing F&I Automotive Reinsurance Models

There are several profit-sharing and reinsurance models, each offering different levels of control, risk, and return:

Retro Profit-Sharing Programs: A simple entry point requiring no upfront investment, but offering limited control and smaller payouts.

Controlled Foreign Corporation (CFC): Dealer-owned offshore reinsurance company with strong control and tax benefits, but limited by premium caps.

Non-Controlled Foreign Corporation (NCFC): A group-owned structure offering tax efficiency and simplicity, though with less dealer control.

Dealer-Owned Warranty Company (DOWC): A domestic entity offering full ownership and maximum profit potential, with higher responsibility and complexity.

Super CFC: An advanced structure removing premium caps and offering scalability and upfront tax advantages, ideal for high-volume dealers.

Understanding and Profiting from Reinsurance Structures

Dealers profit from reinsurance through:

Underwriting Profit: Premium collected minus claims and expenses.

Investment Income: Reserves held and invested generate additional returns.

Tax Optimization: Strategic formations defer or minimize tax, letting profits grow faster.

Fee Reduction: Owning reinsurance eliminates unnecessary third-party fees.

Access to Funds: Profits can be distributed as dividends or even borrowed against for dealership expansion or liquidity needs.

The result is a self-sustaining wealth-building mechanism that strengthens a dealership year after year.

Choosing the Right Formation: CFC, Super CFC, NCFC, and DOWC

CFC: Offshore, dealer-owned, strong control, good for mid-sized dealers.

Super CFC: Scalable, no premium caps, upfront tax advantages, great for high-volume dealers.

NCFC: Group-owned, simple and passive, but with less control.

DOWC: Full control and maximum profitability, ideal for large or aggressive dealers willing to take on more responsibility.

The right formation depends on dealership size, F&I volume, and appetite for involvement.

What Products Can Be Reinsured?

Almost any F&I product can be reinsured, including:

Vehicle Service Contracts

Powertrain Warranties

GAP Insurance

Tire & Wheel Protection

Key Replacement

Appearance Protection Plans

Prepaid Maintenance

Theft Protection, Etching, Roadside Assistance, and more

Every F&I sale can contribute to your long-term wealth through the right reinsurance structure.

What is Warehousing in Reinsurance?

Warehousing is a process where your provider temporarily holds F&I business while your reinsurance company is being formed. Once your company is ready, all warehoused contracts are transferred into it. This ensures you don’t lose months of profit while waiting for setup to complete.

How to Choose Where to Form Your Reinsurance Company

Dealers can form reinsurance companies offshore (e.g., Cayman Islands, Bermuda, Turks & Caicos) or onshore (e.g., captive-friendly U.S. states). Offshore offers lower capital requirements and simpler regulations, while onshore provides domestic credibility and sometimes tax advantages. The best domicile depends on your goals, tax strategy, and advisor’s expertise.

Elite FI Partners – Trusted Partner for Dealers Nationwide

At Elite FI Partners, we specialize in helping dealerships nationwide design, implement, and maximize profit-sharing and reinsurance programs. We tailor solutions to each dealer’s needs, whether that means starting with a simple retro, building a CFC, or leveraging advanced strategies like a Super CFC Reinsurance Program.

We provide compliance expertise, transparent reporting, and hands-on support so dealers can focus on running their stores while we help grow long-term wealth. From program setup to ongoing F&I training and performance optimization, Elite FI Partners is the trusted advisor for dealers who want to take control of their profits.

Ready to stop leaving money on the table? Explore our Dealer Wealth Programs or contact Elite FI Partners today to start your journey toward greater profitability and long-term financial success.

Frequently Asked Questions (FAQ)

Q: What’s the difference between a CFC and a Super CFC?

A CFC is a dealer-owned offshore reinsurance company limited by premium caps. A Super CFC removes those caps, uses retail accounting for upfront tax advantages, and scales better for high-volume dealers.

Q: What does DOWC mean?

DOWC stands for Dealer-Owned Warranty Company. It’s a U.S.-based company owned by the dealer that directly issues F&I products, offering full control and higher profit potential.

Q: What is an NCFC?

NCFC stands for Non-Controlled Foreign Corporation. It’s a pooled offshore reinsurance structure owned by many dealers, offering tax benefits and simplicity but less individual control.

Q: Are reinsurance and profit-sharing programs legal and safe?

Yes. These are well-established, compliant programs when structured properly. Thousands of dealers nationwide use them to grow profitability and long-term wealth.

Q: How do payouts work?

Profits are distributed after claims and reserves are accounted for. Depending on structure, dealers may receive annual or quarterly distributions, or let profits compound tax-deferred until later withdrawal.

Comments