Unlock Explosive Growth: Why Powersports Dealers Cannot Afford to Ignore Profit Sharing

- Michael Dean Aufmuth

- Feb 21

- 6 min read

The Silent Wealth Gap in the Powersports Industry

There is a significant financial gap in the powersports industry that most dealers do not even realize exists.

In automotive, structured profit sharing and reinsurance participation are standard for high-performing dealers. The discussion in that industry is no longer about whether to participate. It is about structure, transparency, and minimizing unnecessary fees. In powersports, however, many dealers are still not participating in any formal profit sharing or reinsurance structure at all.

They are selling powersports F&I products. They are generating premium. They are producing underwriting profit. But they are not retaining it.

That is the silent wealth gap, and right now there is a narrow window of opportunity for dealers willing to act before the rest of the market catches up.

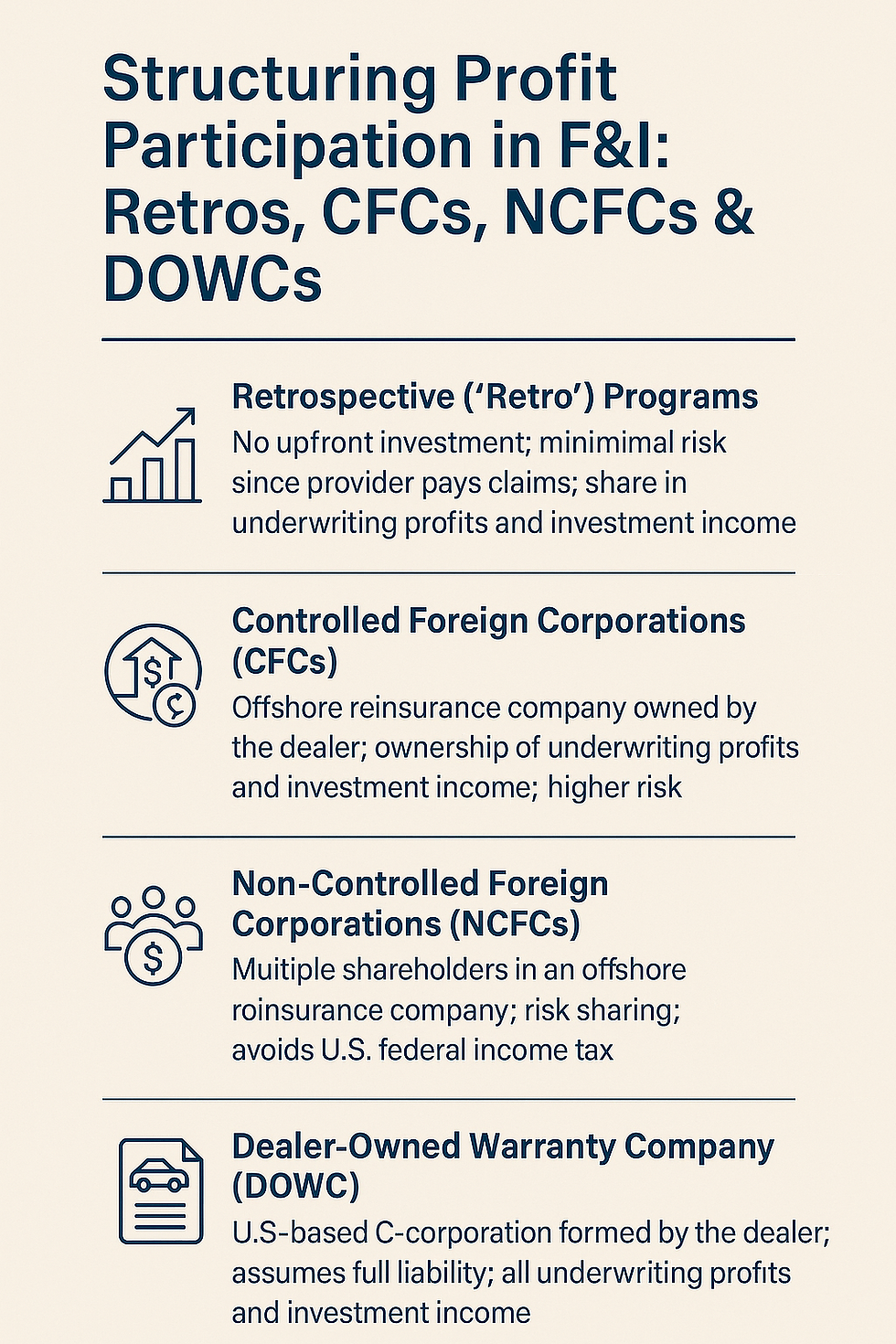

Understanding Powersports Reinsurance as a Wealth Strategy

Powersports reinsurance is often misunderstood. It is not simply an accounting tool or a back-end technical structure. It is a long-term wealth-building strategy.

When properly designed, a powersports profit sharing or reinsurance program allows a dealer to participate in the underwriting performance of the F&I products they sell. Instead of earning commission alone, the dealership builds reserves and retains profit over time. That fundamentally changes the role of the F&I department.

Powersports F&I products such as extended service contracts, GAP protection, tire and wheel coverage, theft protection, and appearance programs already drive revenue and increase PVR. However, when those products are structured within a reinsurance model, they begin creating something far more powerful than monthly income. They begin creating long-term capital.

That capital accumulates. It compounds. It becomes leverage. This is the difference between earning income and building wealth.

The Industry Is About to Shift

Here is where urgency becomes critical.

Many administrators in the powersports space have historically not emphasized profit sharing or structured participation. That reality is changing. As more dealers begin asking informed questions, administrators will respond. They will introduce participation models. They will refine their messaging. They will attempt to protect their portfolios.

When that shift happens, the conversation becomes crowded.

Right now, however, early movers have a distinct advantage. Dealers who establish strong and transparent powersports reinsurance structures today will have more time in the market accumulating reserves. They will maintain stronger negotiating leverage. They will build structural advantages that competitors cannot easily replicate.

Time is one of the most powerful components of reinsurance performance. Delaying participation does not simply delay profit. It delays compounding. And compounding is what builds wealth.

Raising the Standard in Powersports F&I

When discussing profit sharing, many powersports dealers respond with pride about their administrator. They emphasize that their customers are taken care of, that claims are handled properly, and that service is strong.

That should not be a differentiator. That should be the standard.

Strong claims performance and administrative integrity are non-negotiable. A dealer should never sacrifice customer experience for profit. However, once that baseline is met, the next strategic question must be asked: Are we participating in the profit created by our own F&I production?

If the answer is no, then the dealership is funding someone else’s long-term balance sheet.

The objective is not to replace strong administration. The objective is to pair strong administration with structured wealth participation. Customer protection and dealer wealth building should coexist.

How Powersports Profit Sharing Transforms a Dealership

When a powersports dealer implements a properly designed profit sharing program, the financial trajectory of the store begins to change.

Instead of relying solely on monthly gross performance, the dealership builds reserves from underwriting profit. Over time, those reserves create a secondary financial foundation that is less dependent on seasonal cycles and market volatility. This provides stability in an industry that can experience significant swings.

Accumulated reserves also create strategic flexibility. Dealers can reinvest in additional inventory, upgrade facilities, expand marketing efforts, pursue acquisitions, or open additional rooftops. Rather than depending entirely on outside lenders, the dealership develops internal capital resources.

That is real powersports wealth building.

Additionally, a dealership with a well-structured reinsurance program becomes more attractive to potential buyers. Recurring underwriting income, disciplined financial reporting, and accumulated reserves increase enterprise value. Profit sharing is not simply about improving this year’s performance. It is about increasing long-term valuation.

The Connection Between Training and Reinsurance Performance

A profit sharing structure alone does not guarantee strong results.

Powersports F&I product penetration, pricing discipline, and process consistency directly impact reinsurance performance. Without proper training and structured execution, even the best reinsurance design will underperform.

For a powersports reinsurance model to reach its full potential, it must be aligned with a disciplined F&I process, consistent menu presentation, and clear communication of product value. Wealth building requires intentional execution. Dealers who treat F&I as a structured and accountable profit center consistently see stronger reserve growth than those who approach it casually.

The structure matters, but so does the process behind it.

Why Waiting Carries Real Risk

The powersports industry is becoming more competitive. Inventory costs fluctuate. Consumer buying patterns evolve. Margins expand and contract with market cycles.

Dealers who rely exclusively on front-end gross are exposed to these shifts. Dealers who build layered profit strategies are more resilient.

Right now, most powersports dealerships are not fully participating in structured profit sharing. That creates opportunity for early adopters. As awareness increases and more administrators introduce participation models, differentiation will shrink. The dealers who move now will have more years of accumulation, more capital available for growth, and stronger competitive positioning.

There is a finite window before this becomes standard practice across the industry.

The Real Question for Powersports Dealers

The automotive industry underwent this evolution years ago. Reinsurance and profit participation became central to long-term dealership financial strategy. Powersports is following that same trajectory.

Dealers who recognize this shift early will build financial infrastructure that supports expansion, stability, and long-term enterprise value. Dealers who delay will eventually enter the conversation later, with fewer accumulated reserves and less time working in their favor.

The fundamental question every powersports dealer should ask is simple: Are we building wealth from the F&I products we are already selling?

If not, someone else is.

Powersports profit sharing and reinsurance participation are not short-term trends. They represent a structural shift in how dealerships create lasting value. The opportunity exists right now, but it will not remain under the radar forever.

The dealers who act early will not just increase PVR. They will build capital. They will strengthen their balance sheet. They will create expansion opportunities. They will position themselves for explosive growth.

And in an industry where timing matters, that decision cannot be postponed indefinitely.

FAQ

1. What is a powersports profit sharing program?

A powersports profit sharing program is a structure that allows a dealership to participate in the underwriting profit generated by certain powersports F&I products, instead of earning only retail commission. When structured correctly, it creates long-term reserves that support powersports wealth building.

2. What is powersports reinsurance and how does it work?

Powersports reinsurance is a form of profit participation where a portion of premium and underwriting performance is captured in a dealer-owned structure. Over time, the dealer can build reserves from the book of business they create through selling qualifying powersports F&I products.

3. Why are more powersports dealers talking about profit sharing now?

Because the market is maturing. Dealers are asking better questions about where premium dollars go, how administrators are compensated, and how to build long-term value. Dealers also want stronger financial strategies to offset margin pressure and inventory volatility.

4. What powersports F&I products typically fit best for a profit sharing or reinsurance model?

Products with stable loss performance and consistent underwriting tend to fit best. This commonly includes service contracts or vehicle service agreements, limited warranty programs, and certain ancillary protection products depending on claims experience and structure.

5. Why is claims handling still critical if the goal is profit sharing?

Because claims performance impacts customer experience and the long-term performance of the program. Strong administrators protect both the customer and the dealership, and consistent claims outcomes help preserve underwriting results inside a profit sharing or powersports reinsurance structure.

6. How does a powersports reinsurance program support wealth building?

By creating dealer-owned reserves that can grow over time. Dealers can use those reserves strategically to reinvest into inventory, fund expansion, upgrade facilities, or strengthen financial stability through changing market conditions.

7. What is the biggest mistake dealers make when evaluating profit sharing programs?

Focusing only on the participation pitch without fully understanding fees, transparency, reporting, claims management, and how training impacts performance. Structure and execution both matter. Poor design or weak process can silently reduce long-term value.

8. Why does timing matter when a dealer enters a profit sharing program?

Because time in the market matters. The earlier a dealer starts building a book of business in a well-designed structure, the more reserves can accumulate. Waiting often means missing years of compounding and entering later when more providers start offering similar models.

9. Do dealers need training for profit sharing to work?

Yes. Penetration, pricing discipline, and consistent F&I process directly impact the performance of the program. A strong powersports profit sharing or reinsurance model is amplified by training that improves presentation, consistency, and product performance.

10. How can a powersports dealer know if they are in the right structure?

Dealers should review transparency of reporting, fee detail, product performance, claims standards, and how the structure supports long-term dealer wealth building. A side-by-side analysis often reveals whether value is being retained or drained through costs and limitations.

Comments